US-China strategic competition is set to be one of the major drivers of the global economy in the years to come. In recent weeks, disputes over export controls of rare earth-related supply chains almost led to a major escalation of US-China trade conficts. But what are rare earths materials and why are they so important for the global economy and US-China relations?

Despite their name, rare earth elements are not particularly rare in the Earth’s crust. The challenge lies in their extraction and refining, which are technologically complex, environmentally sensitive, and capital intensive. The group includes 17 elements such as neodymium, dysprosium, terbium, cerium, lanthanum, and yttrium, each with unique magnetic, optical, or catalytic properties that make them indispensable for modern industry. In addition, several related critical minerals, including gallium, germanium, indium, cobalt, and lithium, play similar roles across supply chains.

Together, the importance of these materials can be seen most clearly in three of the most important, rapidly expanding sectors in the world. In the field of AI and semiconductors, rare earths are integral to the machinery and processes that make advanced chips possible. Cerium oxide is used to polish silicon wafers with nanometric precision, yttrium is a core component of plasma etching systems, and neodymium-based magnets power the high-efficiency cooling and motor systems used in AI data centers. Meanwhile, related elements such as gallium and germanium are used directly in high-performance chips and optical communications. In defense and aerospace, other rare earths are key inputs for jet engines, radar systems, and precision-guided weapons. Finally, in the energy transition, rare earths like neodymium and paraseodyum are essential for the powerful magnets that make EVs and wind turbines operate efficiently, while lanthanum and cerium play crucial roles in catalytic converters and energy storage technologies.

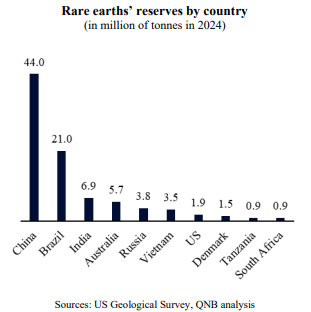

The exponential growth in demand has transformed rare earths and critical minerals from industrial commodities into strategic assets. This growing importance has also created new geopolitical frictions, largely because production and processing capacity are highly concentrated in a few countries, particularly China. While deposits of rare earths are found globally, the refining and separation processes – which turn raw ore into usable materials – are overwhelmingly dominated by Chinese companies.

China’s rise in this field was the result of decades of deliberate industrial policy. China’s leadership recognized early the leverage that such dominance provides. In a now-famous remark, former Chinese leader Deng Xiaoping observed in 1987 that “The Middle East has oil; China has rare earths.” The country invested heavily in geological surveys, mining, and refining technology. By the early 2000s, China had become the dominant player in nearly every stage of the supply chain. Today, it accounts for around 65 percent of global mine output but over 85 percent of global refining and processing capacity. It also produces the majority of the permanent magnets and other high-value downstream products that depend on these materials. The country has also invested in expanding its footprint across the industry overseas, controlling significant assets, resources and reserves even outside China.

In 2021, Beijing consolidated several state-owned companies into the China Rare Earth Group, strengthening its control and coordination over the sector. More recently, China has introduced export controls on national security reasons. Officials have emphasized that these controls are not outright bans but measures to ensure “responsible and secure” trade in dual-use goods. Nonetheless, these steps have reinforced perceptions that China views control over critical minerals as an important element of its broader geopolitical toolkit.

In response, other countries have moved to diversify supply chains and reduce strategic dependence. The US has classified rare earths as critical to national security and is investing in domestic mining and processing through the Defense Production Act. However, these efforts will take years to bear fruit. Refining rare earths is a complex process that involves hazardous waste and high costs, and rebuilding capacity at scale outside China will not be easy. As a result, China is likely to remain the central actor in global rare earth markets for the foreseeable future.

All in all, rare earths were key for the electronics and digital revolution and are becoming even more important as new industries and technologies emerge. AI, semiconductors, defense and aerospace, as well as energy transition are becoming some of the most strategic sectors for the 21st century and should require massive growth in rare earth supply. This further strengthens China’s dominant position in these supply chains and creates bottlenecks as well as vulnerabilities to the US and other competitors.

Download the PDF version of this weekly commentary in English or عربي